Research & Whitepapers

The Micro-Cap Advantage: How MicroCap Equities Have Helped Enhance Return and Lower Correlation in Client Portfolios

The Micro-Cap Advantage

Ever since stock markets were created, investors have been devising schemes to enable them to beat the market’s average return. Some invest in large companies, some invest in small companies, and others ignore company size and invest in companies of any size as long as they have potential to produce market-topping returns. Some investors buy-and-hold while others trade frenetically. Some invest in high multiple growth stocks while others prefer to shop among companies whose stocks have recently been beaten down. Then there are the technical analysts and those who analyze only economic fundamentals. Some investors assemble portfolios from “the top down” while others prefer a “bottom up” approach.

Academics have long admonished investors for spending so much time trying to predict the future. They point to the plethora of studies that indicate the stock market is a reasonably efficient mechanism. In an efficient market, the best guess at tomorrow’s stock price is today’s price. The existence of numerous buyers and sellers and the near instantaneous flow of new information cause securities to be priced according to their inherent risk. Most academics will tell you the only way to produce market-topping long-term investment returns is to build and maintain a highly diversified portfolio that contains more systematic risk than the stock market as a whole. In short, what investors ultimately get from their equity portfolios is paid for by the risks they take.

The Small Firm Effect

The first formidable crack in the so-called efficient market theory appeared in the late 1970s when a University of Chicago doctoral student discovered a strategy that has produced superior investment returns for more than 80 years. Superior meaning that this strategy has historically produced greater returns than dictated by portfolio risk. This strategy has come to be known as “the small firm effect.”

Simply put, the small firm effect is the tendency of the common stocks of small firms to outperform the common stocks of large firms given the same level of risk. In an efficient market, the expected rate of return from any portfolio is directly related to its non-diversifiable risk. The greater the level of non-diversifiable risk, the greater the expected rate of return. Contemporary research, however, indicates that this has not been the case for well-diversified portfolios consisting of small firm common stocks.

The small firm effect was first measured in 1978 by Rolf Banz while completing his doctoral dissertation at the University of Chicago. Banz ranked NYSE-listed stocks by market capitalization and formed five portfolios containing the largest to smallest stocks listed on the Exchange. These portfolios were held for five years and then the stocks were re-ranked and new portfolios were formed. He repeated the process throughout the period 1925 through 1975. Next, he measured the monthly returns of each portfolio and applied a least squares regression analysis to those returns to obtain each portfolio’s beta (measure of relative systematic risk) and alpha (the portfolio’s average monthly risk-adjusted return). He expected portfolios with larger amounts of systematic risk to produce larger investment returns than portfolios with smaller amounts of systematic risk. What he found was a return anomaly that has yet to be fully explained.

- Over the 50-year period studied, the first four portfolios (those containing all but the smallest NYSE firms) provided investors with investment returns dictated by the risk of the portfolio, indicating these portfolios were efficiently priced. (Actually, these four portfolios provided investors with an average risk-adjusted monthly return of -0.06 percent per month (alpha), or -0.72 percent per year, less than they should have given the amount of systematic risk they contained.) These portfolios, if anything, were slightly overvalued by the market during this period.

- On the other hand, the portfolio containing the smallest NYSE companies provided investors with a risk-adjusted excess rate of return of 0.44 percent per month (alpha), or nearly 6 percent per year.

Since Banz investigated the risk/return behavior of only NYSE-listed stocks, he was mute regarding the universality of the small firm effect. However, Professors Thomas Cook and Michael Rozeff of the University of Iowa examined the nature of firm size and investment returns using stocks listed on the NYSE, the AMEX and those traded over-the-counter over the period 1968-1978. They ranked 3,130 stocks on the basis of market capitalization and divided them into 10 portfolios containing an equal number of stocks

- The four portfolios containing the stocks with the lowest market values provided monthly returns of 0.14 to 0.45 percent after adjustment for risk.

- The remaining six portfolios (containing larger company stocks) all possessed negative monthly alphas ranging from -0.01 percent to -0.35 percent.

Thus, the market undervalued small firm stocks during this period and overvalued large firm stocks. The annualized risk adjusted returns for the portfolios of the smallest and largest firms revealed a wide distribution, ranging from 5.4 percent for the decile 10 portfolio (smallest companies) to -4.2 percent for the decile 1 portfolio (largest companies).

During the last three decades, many researchers who doubted the existence of a small firm effect have subjected stocks of small and large firms to numerous tests using various statistical techniques. All confirm its existence, although its explanation continues to be a subject of ongoing debate.

The Small Firm Effect: A Rationale

Whatever the explanation of the small firm effect, it is not because firms are small. Firm size is most likely just a proxy for one or more factors, which highly correlate with firm size. For example, David Dreman popularized the notion that lower valuation multiple stocks tend to outperform higher valuation multiple stocks. It could be that firm size is a proxy for the low P-E ratio effect. However, recent research indicates the reverse – that the P-E anomaly is actually a proxy for the small firm effect.

An examination of the characteristics of small versus large firms reveals striking differences:

- First, the micro-cap segment of the U.S. equities markets is very small. The aggregate market capitalization of the entire micro-cap universe is approximately $309 billion. Of this amount, about $103 billion is in the hands of company founders and their families. That leaves about $206 billion available for the investing public. To put this number in perspective, it is only 35% of the market value of Apple Inc.

- Furthermore, the median market capitalization of stocks in the micro-cap universe is about $301 million. Because of limited liquidity (the average daily trading volume of most micro-caps is usually measured in thousands of shares rather than the millions of shares traded daily for large-cap stocks), it is difficult to buy and sell a large number of shares of micro-cap stocks without significantly impacting share price. As a result, large institutional investors tend to shy away from this sector of the market. The absence of a significant player in this segment of the market could very easily distort the risk/ return characteristics of individual stocks.

Because institutional investors tend to shy away from micro-cap stocks, it is not surprising to find that very few analysts keep tabs on their activities. In the early 1980’s, Professors Avner Arbel and Paul Strebel authored a study entitled “The Neglected and Small Firm Effects.” In this study, the authors tested the notion that the stocks of less researched companies provide greater risk-adjusted returns than more researched companies. Their study of S&P 500 Index companies indicated the less the research concentration, the greater were risk-adjusted returns. When research concentration was coupled with firm size, the favorable risk-adjusted returns were magnified. While small firms outperformed large firms during the study period, under-researched small company stocks performed even better. In other words, the absence of analyst attention distorts the risk/return characteristics of small firm stocks.

- Another characteristic of small firm stocks is that a significant percentage of their outstanding shares are held by operating management. On average, about one-third of the outstanding shares of companies in the bottom 20 percent of NYSE listed companies (when ranked according to market capitalization) are held by operating management. The next 20 percent have less than 5 percent of their shares in the hands of operating managers. That has led some theorists to suspect that a possible explanation for the small firm effect is that the managers of small firms care about share price performance over the long run because they are such large shareholders themselves. The bulk of their wealth is determined by the price of the shares of stock of the companies they manage. In other words, the objective of outside investors and that of corporate insiders coincide (i.e., maximize the firm’s share price).

As pointed out earlier, the smaller the company the less liquid is its publicly traded stock. That means investors must pay a higher price or receive a lower price when selling large blocks of small firm stocks. As a result of the increased liquidity risk inherent in small stocks, investors may require a liquidity premium to invest in them. In other words, beta may not capture all of the risk inherent in small firm stocks, and the extra returns provided by small firm stocks may be nothing more than payment for liquidity risk. Of course, liquidity risk can be mitigated by those who invest in relatively small amounts of a company’s outstanding shares and those who hold their investments longer term.

- Finally, small firms tend to be under-diversified. While most large firms offer multiple product lines or services, small companies tend to be rather narrowly focused. Because of the lack of product diversification, small companies possess a higher degree of unsystematic risk than do large companies. While a high degree of unsystematic risk may be bothersome to company management, it can be diversified away by investors who maintain well diversified portfolios. On the other hand, large company diversification comes with attendant costs. Thus, it may well be that the superfluous diversification practiced by almost all large companies reduces investment returns more than investment risk. The result is a lower risk-adjusted return than is the case for portfolios that contain the stocks of smaller, more streamlined, firms.

Smaller Company Stocks Have Performed Best

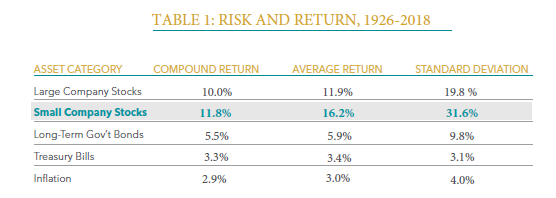

Since 1983, Ibbotson & Associates has reported on the historical returns of various categories of assets. Their initial volume of the Stocks, Bonds, Bills and Inflation Yearbook traced the annual returns of stocks, bonds and Treasury bills back to 1926 and they have updated the monthly and annual returns for these categories ever since. As can be seen in Table 1, the compound annual return of small company stocks has surpassed that of large company stocks (defined as the total annual return of the Standard & Poor’s 500 Index) during this period. The 2.1 percent compound annual return differential favoring small company stocks is by no means a trivial amount. A hypothetical $1.00 investment in the S&P 500 Index made at the beginning of 1926 would have grown to $6,035 at the end of 2016, while a similar hypothetical $1 investment made in a portfolio of small firm stocks would have grown to $33,212. That’s over a five-fold advantage for smaller company stocks.

Small company stocks possess significantly more risk than do large firm stocks. Their annual standard deviation is nearly two-thirds larger than that of large firm stocks. Over relatively short periods of time, small company stock portfolios can experience significant losses. During 1937, the worst year ever for small firm stocks, they lost 58 percent of their value. Furthermore, during the five-year period ending in 1932, small company stocks declined by an average of 27.5 percent a year, representing a plunge of 80 percent. However, all seasoned investors know the potential for larger investment returns are invariably accompanied by larger investment risks.

While small company stocks have historically outperformed large company stocks over the long run, they may not do so during relatively short periods of time. During 34 of the last 89 years, for example, large company stocks provided larger returns than small company stocks. But even over relatively short time periods such as one-year, the odds of achieving over performance favor small firm stocks. That is, during the last 89 years, small company stocks topped the returns of large company stocks in 55 years or 62 percent of the time.

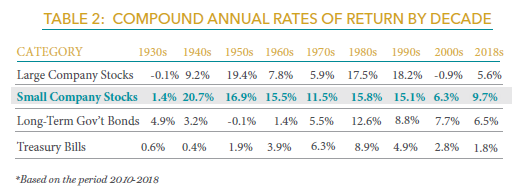

Table 2 lists the compound annual returns of four categories of investments by decade since the 1930’s. As can be seen, during three of the last seven decades, large company stock returns exceeded those of small companies. Although small company stocks performed exceptionally well during the decades of the 1980’s and 1990’s (average compound annual return in excess of 15 percent), large company stocks performed even better. However, that exceptional performance came to an abrupt halt in early 2000 when the air was let out of the internet/technology balloon. In fact, during the ten-year period ending 2010, small company stocks returned a cumulative total of 150.10 percent versus a cumulative 14.92 percent total return for the Standard & Poor’s 500 Index.

Although portfolios of small firm stocks are risky, their compound annual returns during each of the last seven decades have been positive. That is, had you invested in a diversified portfolio of small firm stocks on the first day of each decade and liquidated your investment on the last day of the decade you would never have experienced an investment loss. Furthermore, it is interesting to note that the average returns from Treasury bills did not top the average returns of small firm stocks during any of the last seven decades. In other words, while a small firm stock portfolio experiences significant volatility over short-term periods, some of that volatility can be mitigated by holding a small firm stock portfolio for a lengthy period of time.

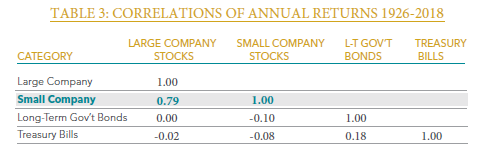

Table 3 illustrates the cross correlations of annual returns for four investment categories. Note that the correlation between small and large company stocks is 0.79. That implies that while the returns of small-cap and large-cap stocks tend to move in similar directions, they do not do so in lockstep. In fact, the percentage of volatility in small-cap portfolio returns that is attributable to the volatility in the stock market as proxied by S&P 500 Index returns (R-squared) is 62 percent. That suggests that there are diversification benefits to combining portfolios of small firm stocks with portfolios of large firm stocks.

Using the standard deviations of small- and large-cap returns illustrated in Table 1 and the correlation coefficient illustrated in Table 3 we can estimate the historical beta for the small-cap portfolio. (This can be done by dividing the annual standard deviation of small-cap returns by the annual standard deviation of the S&P 500 Index returns and multiplying by the correlation coefficient.) This calculation produces a beta of 1.26 versus a beta of 1.00 for the S&P 500 Index. In other words, in standard deviation terms, small stocks are about 60 percent more risky than large stocks. However, they are only about 26 percent more risky in terms of beta risk. If you were to assemble a portfolio that contained one-third of your capital invested in small firm stocks and two-thirds invested in large firm stocks, the weighted average beta of your portfolio would be 1.09 (i.e., a 9.0 percent increase in beta risk versus an all large firm portfolio). However, that portfolio would have an average annual return potential of 13.6 percent. (This is done by multiplying the average annual return of large company stocks of 12.1% by 2/3, multiplying the average annual return of small company stocks of 16.7 by 1/3, and adding the sum). This is a 12.6 percent increase in return potential over the all large company portfolio return of 12.1%. Since return potential (12.6% increase) has increased more than the portfolio’s beta risk (9.09% increase), the portfolio’s risk per unit of return has actually decreased. This is a compelling reason to allocate a portion of any growth-oriented portfolio to small firm stocks.

Small-Cap versus Micro-Cap Stocks

Shortly after the publication of Banz’ seminal research, academics dubbed the extra risk-adjusted returns provided by small firm stocks “the small firm effect.” Small firms were defined as those of all public companies with market capitalizations below that of the company that separated the bottom 20 percent of NYSE-listed stocks from the remainder when ranked from largest to smallest on the basis of equity market value. However, that definition would not stand the test of time.

A dozen years after Banz’ stunning discovery, numerous professional investors sought to capitalize on the small firm anomaly. From a mere handful of small company mutual funds existing in the early 1980’s, the number of small firm mutual funds grew to nearly 100 by the mid 1990’s. However, mutual fund managers soon learned that managing small company assets is no easy task. As cash flowed into their portfolios, many funds were forced into making investments in the stocks of larger, more liquid companies.

- As a result, the small firm mutual fund category was broadened to include funds with average market capitalizations ranging from as little as $50 million to as much as $1 billion. To account for the huge range in average market caps, mutual fund data services coined a new term to separate funds with modest average market capitalizations from those with hefty market capitalizations. Thus, was born the micro-cap fund designation.

Using the definition in the original Banz Study (the bottom quintile or deciles 9 and 10), a small-cap firm today is one whose market capitalization falls below $549 million. However, these are now considered to be micro-cap stocks. In general, the small company designation is considered to be companies with market capitalizations ranging from $549 million to $2.5 billion.

The micro-cap universe contains the stocks of about 1,350 companies with an aggregate capitalization of about $309 billion. (The median market capitalization in the micro-cap sector of the market is approximately $333 million.)

- Although micro-cap stocks encompass more than one-half the number of companies whose stocks are nationally traded, they account for about 1.4 percent of the market’s total market value.

- On the other hand, the 185 largest nationally traded companies have an aggregate capitalization of about $14.8 trillion and account for about 64 percent of the aggregate market value of all publicly traded stocks. The largest publicly traded company, Apple, Inc., has a market capitalization of $591 billion, nearly twice the size of the market value of the entire micro-cap sector.

The arithmetic mean annual return for the smallest stocks (deciles 9 and 10) is significantly larger than that of the largest nationally traded stocks (deciles 1 and 2). The absolute difference in arithmetic mean return between decile 1 and decile 10 stocks is indeed impressive (20.6 percent versus 11.2 percent).

However, the true micro cap advantage lies in the fact that on a risk-adjusted basis, diversified portfolios of very small company stocks historically have provided returns that exceed those predicted by their relative systematic (beta) risk. Furthermore, the smaller a portfolio’s market capitalization the greater is the return premium.

- Research indicates that micro cap stocks, in aggregate, provide annual returns in excess of those predicted by the Capital Asset Pricing Model that average approximately 3.69%. In other words, portfolios of micro cap stocks have a high probability of producing a significant positive alpha.

The volatility of return in this sector may be more than most investors can tolerate. However, given the superior returns they have historically provided and the relatively low degree of correlation with other equities (most notably large company stocks), it can make solid investment sense to allocate a portion of all growth seeking investors’ portfolios to microcap stocks. The size of such an allocation is open to debate.

These academic findings illustrate the risk-adjusted excess return potential that exists in the micro-cap sector of the U.S. equity market. The “small firm effect” is the tendency of common stocks of small companies to outperform the common stocks of large companies given the same level of risk. Finally, the old investment axiom that investors only get from their portfolio what is paid for by the risks they take can be put to sleep. Here is an academic discovery that for 88 years has delivered returns greater than dictated by portfolio risk.

In Summary

Small company stocks topped the returns of large company stocks in 55 of the past 89 years, or approximately 62 percent of the time. There are several reasons why the small firm effect prevails in the equities market, and they should be considered when constructing a small stock portfolio:

- The micro-cap segment of the U.S. equities market is very small. Approximately $309 billion in micro-cap stocks are available for the investing public, an amount that is only 35% of the market value of Apple, Inc.

- Neglected asset class Less researched companies have proven to provide greater risk adjusted returns than more researched companies. In the absence of significant analyst attention, risk/reward characteristics for micro-cap stocks have become distorted.

- Shares held by company management On average, about one-third of the outstanding shares of micro-cap companies are held by operating management. The objective of outside investors and that of corporate insiders coincide, maximizing the firm’s share price.

- Liquidity risk and long term holding As a result of the increased liquidity risk inherent in small stocks, investors may require a liquidity premium to invest in them, and the extra returns provided may be nothing more than payment for liquidity risk. This can be mitigated by holding investments for a long period of time.

- Streamlined firms and portfolio diversification Smaller, more streamlined firms avoid the superfluous diversification practiced by large companies that reduces investment returns more than investment risk. The result is a higher risk-adjusted return for small stock portfolios, along with a high degree of unsystematic risk. While that risk may be bothersome to small company management, it can be diversified away by investors who maintain well-diversified portfolios.

History demonstrates that small companies have provided superior absolute and risk-adjusted returns compared to large companies over the same time period. The volatility of return in this sector may be more than most investors can tolerate, and small companies do not encompass a complete investment program for these investors. However, given the superior returns small company stocks have provided and their relatively low degree of correlation with other equities, including large company stocks, it can make solid investment sense to allocate a portion of all growth-seeking investors’ portfolios to small and micro-cap stocks.