Research & Whitepapers

Deja vu All Over Again: Serial Correlation and Micro-Cap Equities

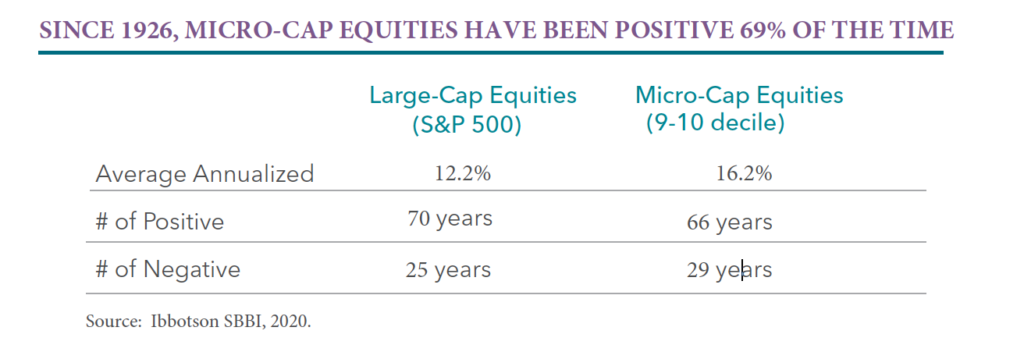

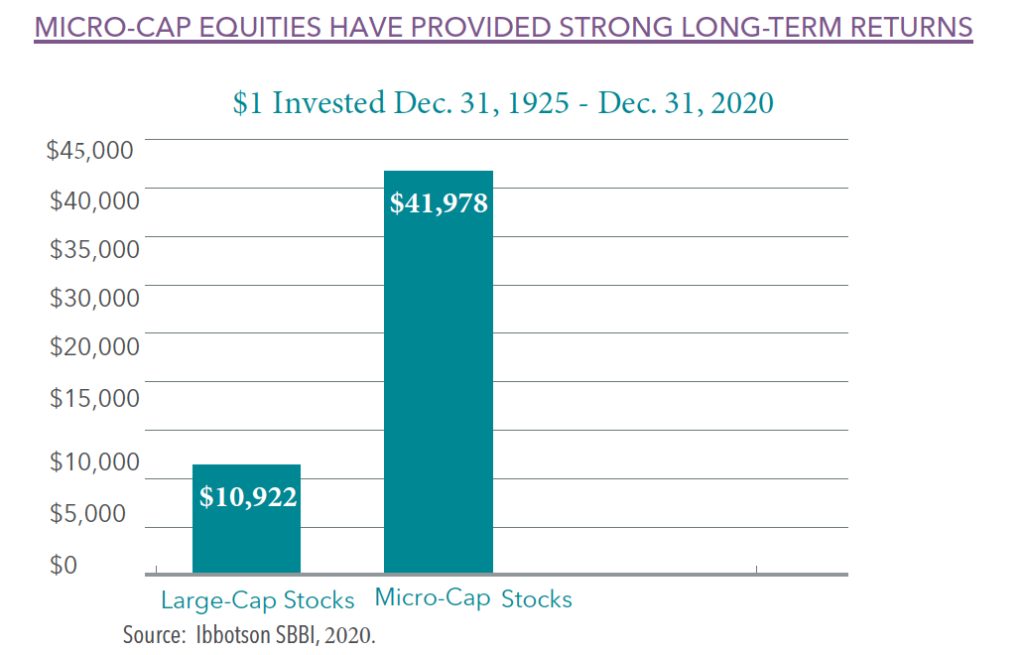

Experienced investors understand how compounded returns can have a significant effect on wealth creation. However it takes more than a little resolve to reap the full rewards of compounded returns, as equities have declined approximately 50% not once but twice in the past fifteen years. Despite these periods of steep decline, equities – particularly micro-cap equities – have provided patient investors with large rewards over the long term. Understanding historical trends in market returns might help investors gain the perspective needed to make investing for the long term an easier pill to swallow.

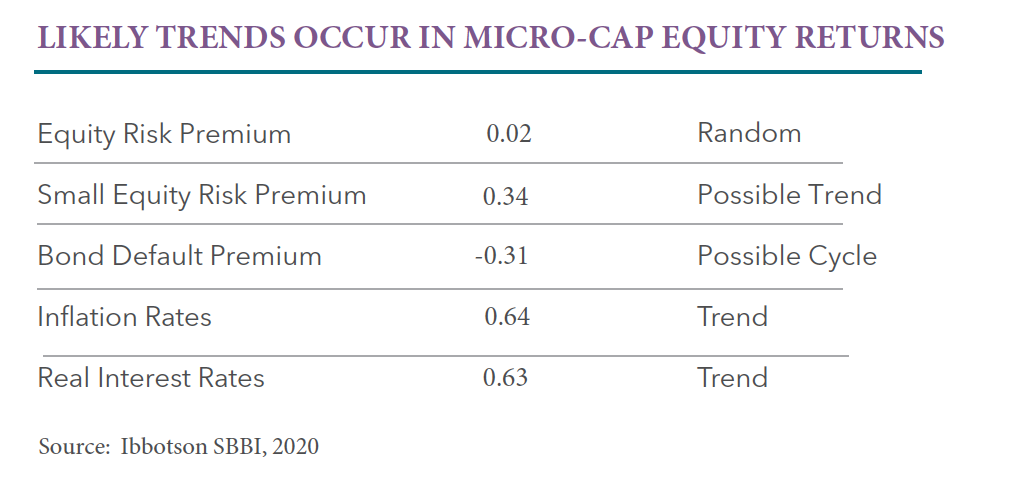

Historical performance trends show that positive and negative returns tend to be grouped together. To understand if there are trends within stock performance, we turn to a statistic terms called serial correlation. The serial correlation of a return series describes the extent to which the return in one period is related to the return in the next period. A return series with a high (near one) serial correlation is very predictable from one period to the next, while one with a low (near zero) serial correlation is random and unpredictable. In the table below, we provide serial correlation for equities, bond defaults, inflation rates and real interest rates. The results show that large equities returns do not show predictive results, ie., their performance is purely random. However, while micro-cap equities returns are of course not purely predictive, there is a likely trend of serial correlation that has been observed within their historical performance.

Historical performance trends show that positive and negative returns tend to be grouped together. To understand if there are trends within stock performance, we turn to a statistic terms called serial correlation. The serial correlation of a return series describes the extent to which the return in one period is related to the return in the next period. A return series with a high (near one) serial correlation is very predictable from one period to the next, while one with a low (near zero) serial correlation is random and unpredictable. In the table below, we provide serial correlation for equities, bond defaults, inflation rates and real interest rates. The results show that large equities returns do not show predictive results, ie., their performance is purely random. However, while micro-cap equities returns are of course not purely predictive, there is a likely trend of serial correlation that has been observed within their historical performance.

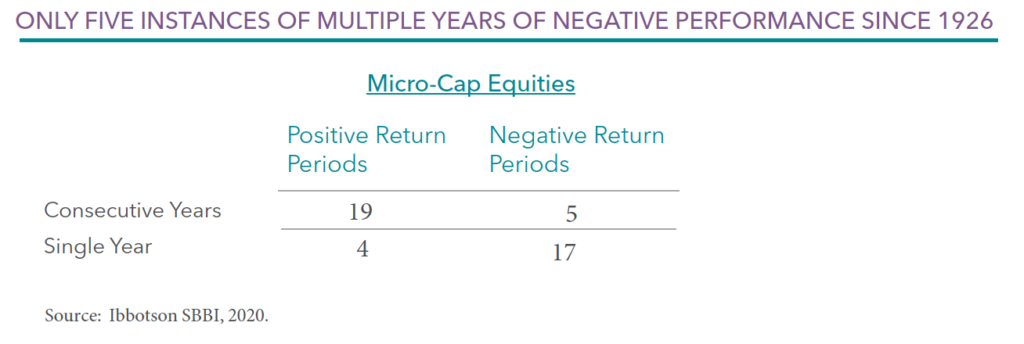

We gathered 95 years of performance in micro-cap equities and grouped them into single-year and consecutive-years performance periods in the table below. (see methodology below*). We found that there were three times as many periods where micro-cap equities experienced a winning streak than period where positive returns lasted only one year.

Overall the 45 periods analyzed, negative returns do not occur in back to back years often, while positive returns do often occur in consecutive years. There were only 5 consecutive-year periods where performance was negative (four periods lasted two years and one period lasted four years). There were 19 periods in which micro-cap equities rose for two or more years in a row. Of the 19 consecutive-year periods of positive returns, 6 lasted two years, 4 lasted three years and 6 lasted four years or more.

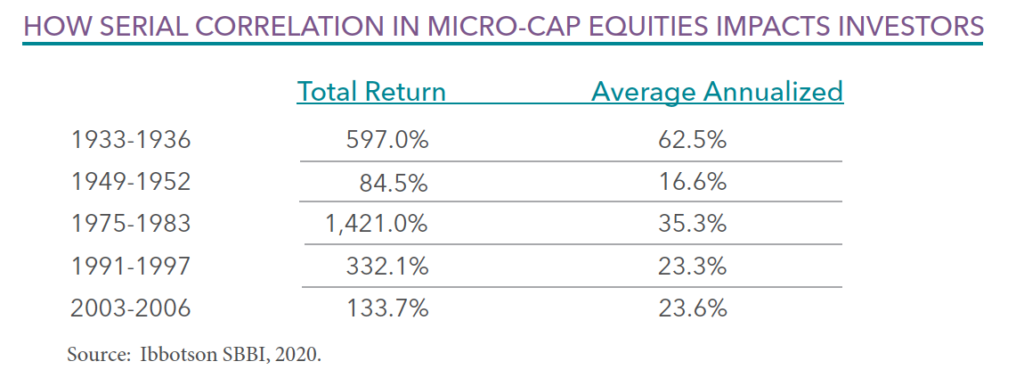

The annualized and total return performance of the five periods which lasted four or more years are listed above. This type of serial correlation to the upside demonstrates why many patient investors have earned significant rewards, notably in the micro-cap equities.

*For example, micro-cap equities had a negative return in 1937, positive returns in 1938 and 1939, negative returns in 1940 and 1941 and then a string of positive returns from 1942 to 1945. This example includes four distinct performance periods: one single-year period of negative returns (1937), two consecutive-year periods of positive returns (1938-39, 1942-45) and one consecutive-year period of negative return (1940-41).