Manager Commentary-Archive

Manager Commentary, 2nd Quarter 2018

2nd QUARTER REVIEW

As stated in our fourth quarter 2017 commentary, we believed the tax cuts would benefit small-cap stocks. This benefit has been the case for some names following recent results, but not all companies. We also stated in that commentary that since several companies have operations around the world and some have deferred tax assets that need to be adjusted or written down, the adjustments to earnings estimates is not simple. This prediction has turned out to be the case across the small-cap universe after the recent round of reports. As we said in the first quarter commentary, the market was a bit of a Jekyll and Hyde type of period, which was characterized first as low volatility and momentum to explosive volatility and fundamental driven market. We are now seeing an even different kind of market, which we will discuss later in this commentary.

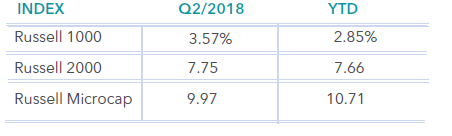

Volatility has certainly increased in 2018, but net results is that smaller stocks have been the leaders. As can be seen in the table below, small stocks beat large stocks and microcap stocks beat small stocks. With the uncertainty of the Tariff impact on the economy and strengthening dollar, investors grew more interested in placing bets on smaller stocks during the past quarter. We believe these two factors drove the superior performance for small and micro-cap stocks in the second quarter.

Past performance does not guarantee future results. Index performance is not indicative of fund performance. To obtain fund performance, click here: https://www.perrittcap.com/funds/

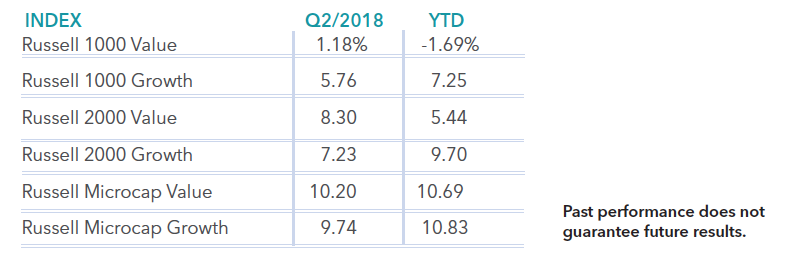

With a strong U.S. economy, one would think value would outpace growth stocks, but it was a mixed performance for large stocks versus small stocks. Value stocks outperformed growth stocks for small- and micro-cap stocks, but the degree was very modest. The table below shows that growth bested value for large stocks by a wide margin. As measured by the Russell 1000 Growth and Russell 1000 Value Index, growth stocks outpaced value stocks by 4.58% during the second quarter. The main reason that growth outperformed was the continued strength of FAANG stocks (Facebook, Apple, Amazon, Netflix and Google). The breadth of the overall market remains very mixed. As measured by the Russell 2000 Value and Russell 2000 Growth Index, value stocks modestly outperformed growth stocks during the second quarter, but growth stocks remained solidly ahead for the year-to-date period. The results are similar for the Russell Microcap Value and Russell Microcap Growth Indexes, but the margin of outperformance for growth stock is only modest for the year-to-date period.

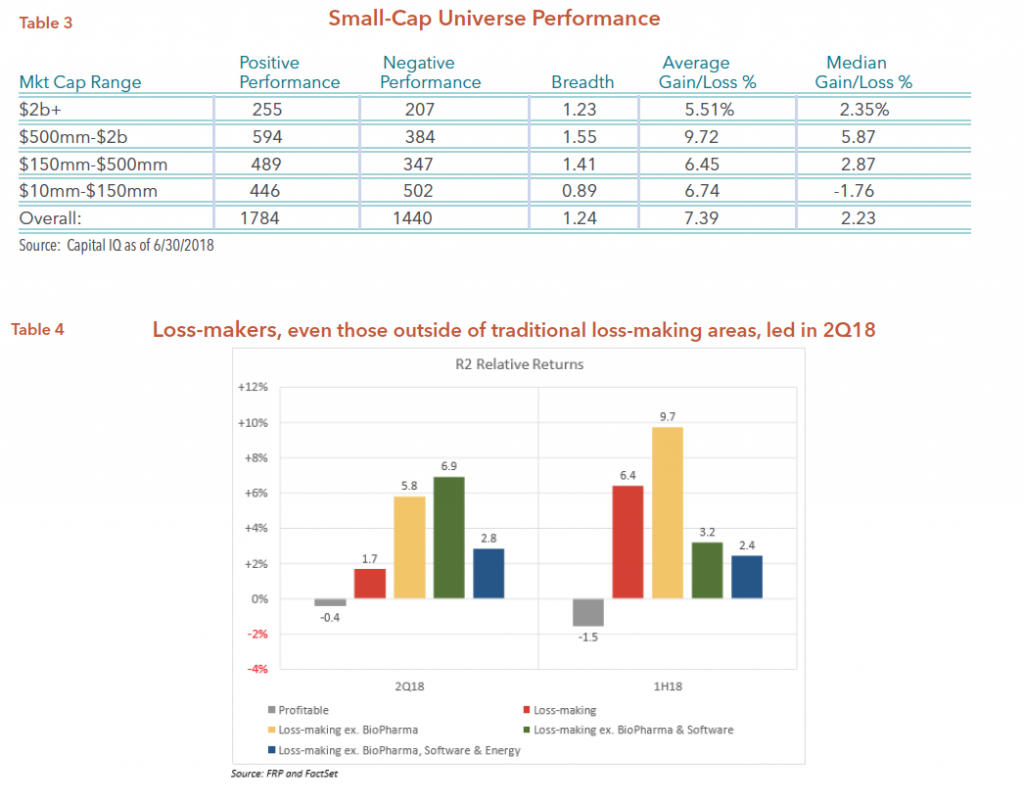

We believe the most interesting data are in the following two tables. These tables give us a better indication of the overall market strength and how quality is performing. As you may know, we measure quality of companies by the level or degree of profitability. As you can see from Table 3, the breadth of the overall market is positive, but the degree is not too strong. Given the high single digit gains from all the indexes in the past quarter, one would think the breadth would be even stronger. Our friends at Furey Research supplied us with Table 4, which tells us this rally in the past quarter was dominated by very low quality stocks. As you can see from the table, profitable companies within the Russell 2000 Index were down 0.4% in the second quarter and finished down 1.5% for the year. On the other end of the spectrum, loss-making (not profitable) companies saw their stock prices climb 6.9% during the past quarter.

We believe this low quality rally may be related to the recent strength in the bond market as well as the recent strength in the U.S. dollar. Low interest rates tend to help risk assets. The yield on the 10-year government bond has recently declined from just over the 3% level to the 2.8% level and the dollar climbed by 5.5% relative to the Euro. We argue this strength in the bond market and the dollar are both short-term in nature. Some of the factors that influence this strength are lower tax rates, particularly for U.S. corporations that were bringing dollars home from overseas markets. We estimate that more than $300 billion was returned to the U.S. market for U.S. corporations. We also argue that the 3% level for the 10-year bond is an attractive level for many investors. We believe, however, that investors will be disappointed due to our belief that higher rates may be in store later this year, as well as next year.

The U.S. economy continues to strengthen, and most indicators such as the Leading Economic Indicator (LEI) show no signs of the economy faltering any time soon. Recent reports show that inflation is rising. Our friends at Furey Research argue that the recently passed tariffs may produce greater inflation. We believe Jim Furey brings up some very important points about tariffs and the markets. Below is an excerpt of his thoughts on this subject. Enjoy!

So what gives with tariffs and investors? What could the consensus be getting wrong when it comes to tariff worries? We have a theory about how the imposition of tariffs could be bullish for stocks and bearish for bonds. It makes a great deal of sense to us, the more we consider it.

Could it be that the way the press and main street financial commentators think about tariffs is totally incorrect? We think maybe. Certainly, the press, which disdains Trump, has a reason to view them bearishly. But the source of the tariff misunderstanding runs deeper.

Living U.S. investors and commentators tariff experience is theoretical and different from their education. Text books taught today’s U.S. investors everything they know, or think they understand about tariffs. The consensus believes tariffs led to the 1930’s Great Depression. But is that true? If you ask Ben Bernanke that question, he will answer, I believe that tariffs were not an economic positive, but it was the highly restrictive monetary policy that caused the Great Depression. If Bernanke is correct, and we suspect he is, there are several questions to ask that might shed light as to why stocks are doing well today in the face of imposed tariffs.

Question 1. What are tariffs’ primary economic impact? First and foremost, tariffs raise the price of imported goods. That creates a pricing umbrella that allows domestic firms to raise price and presumably profits if their own costs don’t escalate. Stop for a moment. Ponder the prior sentence. Tariffs allow domestic companies to raise prices and if costs don’t increase to post higher profits. The press and many commentators are not talking about that outcome.

Question 2. What does the domestic economic, indeed the global economy require, to normalize interest rates, to drive tax revenues and to service government debt levels? You got it. Inflation is required. Stay with me. If tariffs don’t damage the U.S. economy enough to slow growth because the economy is being stimulated by tax cuts, deregulation and improved sentiment, might it be that tariffs are bullish because they lead to higher profits for domestic companies? It’s true that small-caps, which are heavily domestic, are leading. One of the most consistent positive small-cap correlations we monitor is inflation expectations. You have seen us comment on it many times. In light of our earlier comment that tariffs’ primary economic impact is to increase inflation, let’s examine investor inflation expectations through the lens of TIPs spreads versus U.S. government 10-year bond prices.

Question 3. Will the Fed respond to tariff’s higher inflation by hiking faster and repeating the 1930s mistake hiking during a time of rising tariffs? We don’t believe the Fed will choose to hike continually if tariffs continue to rise, especially with weakening overseas economies. We don’t deny that tariffs slow growth on the margin due to higher prices. Remember, Fed officials are human and have emotions. The new Fed chair does not want to be remembered as the chairman who hiked into rising tariffs as overseas growth slowed. It would repeat the 1930 mistake.

Our point today is that the incremental slowdown due to tariffs in todays U.S. economy won’t be sufficient to slow growth below investors’ expectations. In fact, the consensus thought about tariffs’ danger has greatly exaggerated the impact of existing and discussed tariffs place on a $20 trillion-dollar economy. To be sure, the $34 billion of Chinese tariffs announced to match the U.S. imposed sanctions impact less than 2.5% of the U.S. economy.

We foresee a day in the next six months when the Fed, fearing slowing growth overseas and tariffs impact indicate they are pausing or complete in their quest normalizing rates. If that occurs, it will change fixed income investors playbook immediately. While the Fed has been “normalizing” the fixed income investors winning playbook has been to sell the curve’s short end and go long the long end. As soon as the Fed says it will halt normalizing that means the playbook reverses. Fixed income investors will buy the short end and sell the long end. That will immediately steepen the yield curve.

When the Fed says they are done or pausing in their normalization the steeping yield curve will indicate rising growth, in our view. Small-cap portfolios overweight cyclical industries are positioned for that day to arrive. Algo investors will react by buying stocks in such an environment unless the pause is accompanied by a Fed warning on U.S. growth. Recall my wording. The Fed will say they are pausing due to overseas weakness and uncertain tariff impacts. They won’t be pausing, in our view currently, due to weakening U.S. growth.